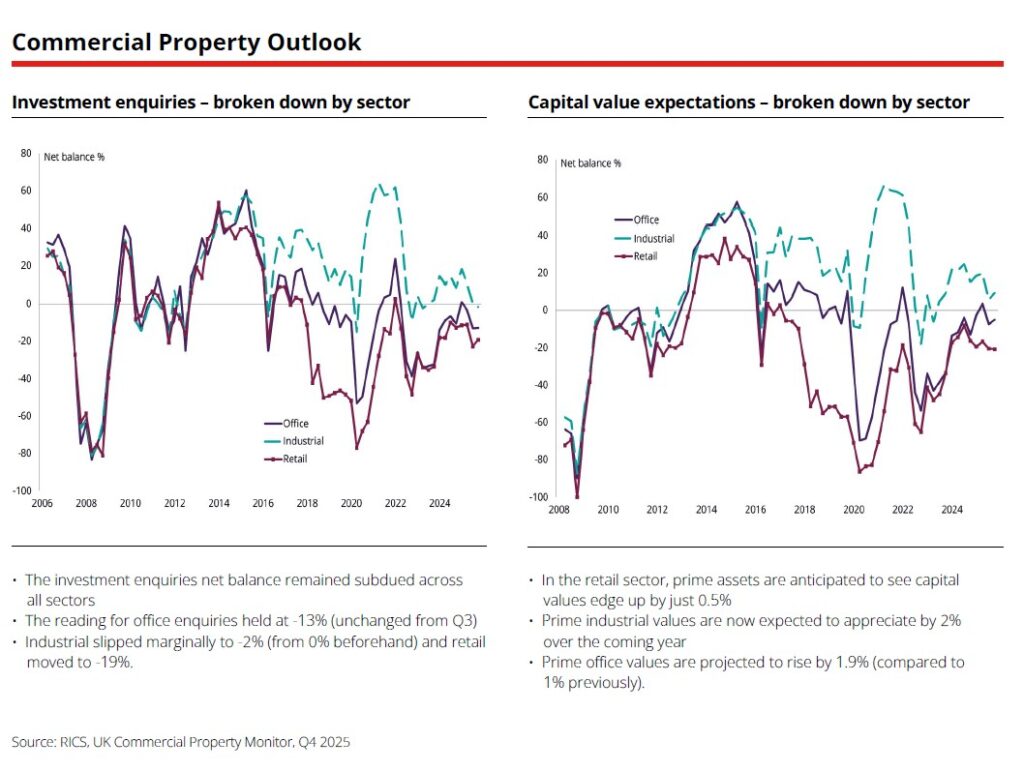

Commercial Property Review – March 2026

| Office demand strong in London – research shows increased activity in the capital, reflecting shift back to office working | Industrial and logistics sector – according to Knight Frank the sector appears to be entering a more stable phase | Life sciences – figures from CBRE indicate total take-up was almost three times the level recorded in H2 2024 |

Strong demand for Central London offices

Investment into the Central London office sector has surged as more companies implement return-to-office mandates.

According to research from BPS London, the office sector was one of the strongest-performing commercial property asset classes last year. This was driven by increased activity in Central London, where office investment rose by 45.1% annually, increasing from £4.79bn to £6.95bn. This reflects a shift back to office-working after the pandemic, with demand for office spaces rising in London. As a result, office rents have gone up in the capital’s most desirable locations, reaching £185 per sq. ft. in the West End. Interestingly, transaction levels across the office sector have fallen by 6.9%, suggesting that investors are becoming more selective, targeting premium spaces that make office-working more appealing. The focus on high-quality offices may make it difficult for smaller businesses to afford spaces in London in future, as they risk being priced out of the market.

Industrial and logistics sector update

What can we expect from the industrial and logistics sector this year? Knight Frank has shared its predictions.

The sector appeared to be entering a more stable phase at the start of 2026, with Knight Frank forecasting an increase in core capital investment due to improved investor confidence. This was expected to be supported by decreasing debt costs, however the outlook has become more uncertain due to the economic impact of the war in Iran. Overall, any growth is likely to be driven by rental income and a modest rise in property value, rather than yield compression.

In the occupier market, demand was resilient in 2025, with UK take-up increasing by 13% year-on-year, reaching 40.8 million sq. ft. The average transaction size rose by 8% annually, reflecting heightened demand for higher-spec buildings that are automation-ready. Occupier demand is expected to stabilise further this year, with operators continuing to prioritise the efficiency of a building.

How is life sciences performing?

Figures from CBRE offer an insight into life sciences activity across the UK Golden Triangle.

The Golden Triangle refers to the life sciences cluster encompassing London, Cambridge and Oxford. In H2 2025, total take-up was 633,700 sq. ft., almost three times the level recorded in H2 2024. This brought take-up for the whole year to 889,800 sq. ft., with Oxford accounting for 75% of this.

Oxford was also the only market that recorded any investment activity in the second half of last year, with just over £1bn transacted. This is well above the average level of £0.38bn, driven by the £890m sale of Oxford Science Park. Cambridge and London did see notable investment activity in H1 2025.

More life sciences space is in development – at the end of 2025, 3.6 million sq. ft. of space was under construction across the Golden Triangle, expected to be complete by the end of 2028.

Hotel sector regains momentum

Figures from Colliers show that the hotel sector got off to a relatively strong start to the year.

In January, £550m was invested into UK hotels – this is significantly higher than the five-year monthly average of £300m and more than seven times the total for January 2025 (£70m). This comes after a strong finish to 2025 for hotels, which suggests that the upwards momentum is being maintained. In the second half of last year, revenue per available room rose annually by 4.4% to £236. Meanwhile, hotel occupancy rates increased by 1.9% to 86.5%, reflecting an increase in demand for wellness and leisure.

The challenge for the hotel sector is that its performance is often measured by short-term indicators. To sustain investor interest, hotels may need to place greater emphasis on longer-term measures – for example, multi-year corporate relationships provide reliable income streams, thus enhancing investor confidence.

All details are correct at the time of writing (24 March 2026)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.